Oil Market Monitor - Geopolitics drive volatility amid supply glut

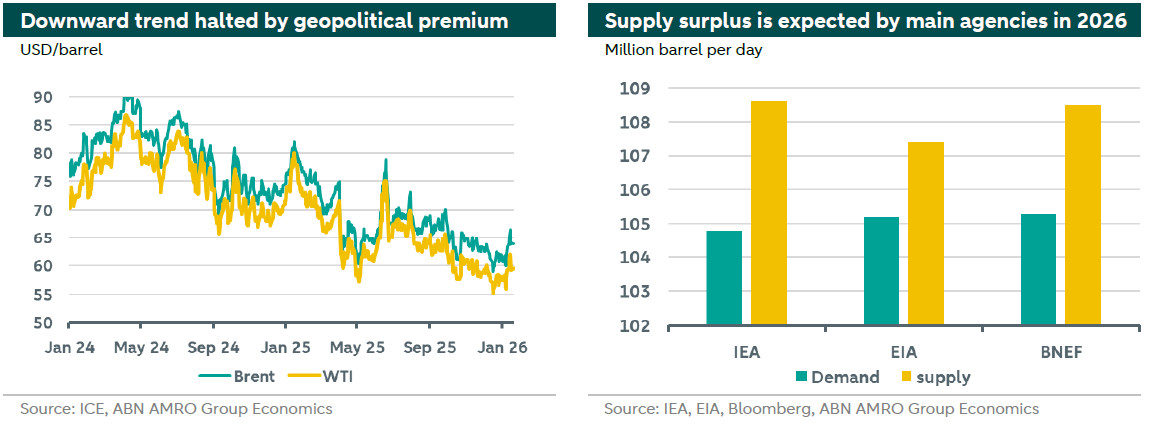

The downward trend in oil prices was reversed in 2026 as markets responded to rapid geopolitical developments. The overthrow of Venezuela's leadership, new U.S. sanctions on Iran, ongoing threats against the Iranian regime, and the slow progress in peace negotiations to end the war in Ukraine have all contributed to an increase in the geopolitical risk premium for Brent crude prices. Despite these pressures, the surplus in oil supply has helped to cap further price increases. Meanwhile, OPEC+ has maintained its decision to pause production increases for the first quarter of the year. Global demand has proven more resilient than anticipated, though the outlook remains clouded by growing tensions between the U.S. and the EU over Greenland, including the potential for new U.S. tariffs and possible EU retaliation. Given the rising geopolitical uncertainties and the dynamic nature of recent events, we choose to leave our outlook unchanged for now. At the time of writing, Brent crude is trading at $64.1 per barrel.

Rapid geopolitical events, including Venezuela’s leadership change and US sanctions/threats against Iran, added $4–$7 per barrel to Brent prices

OPEC+ confirmed its decision to pause production increases for Q1 2026, while agencies forecast a growing surplus

US-EU tensions over Greenland and possible new tariffs across the Atlantic would lower oil demand growth and worsen the surplus

Given the high level of uncertainty, our outlook remains unchanged, though the market will be highly sensitive to geopolitical developments that could alter forecasts

Oil market dynamics

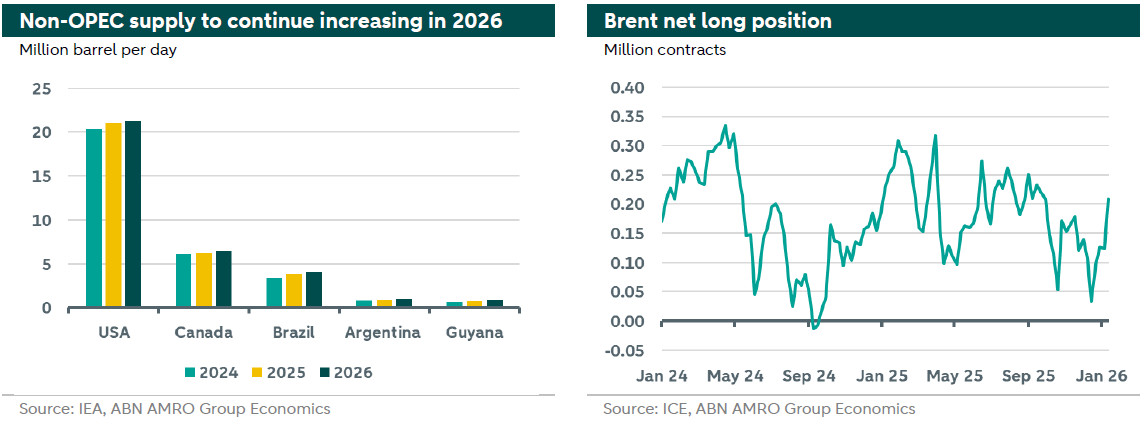

On the supply side, OPEC+ has reaffirmed its decision to halt production increases for the first quarter of 2026. During a virtual meeting held on January 4 with eight member countries, the group emphasized its commitment to maintaining market stability. However, it also stated that the remaining voluntary cuts of 1.65 million barrels per day (extra voluntary adjustments announced in April 2023) could be reinstated, either partially or fully, depending on how market conditions evolve, and this would be implemented gradually. The eight key members of OPEC+ have about 1.2 million barrels per day of their current supply allocation left to restore. On the other hand, production by non-OPEC producers is expected to continue growing throughout 2026. Output reached record levels in 2025, particularly in the United States, Canada, Brazil, and Guyana (see left graph below).

Leading agencies, including the International Energy Agency (IEA), the Energy Information Administration (EIA), and BloombergNEF (BNEF), have maintained their forecasts for a supply surplus in 2026 in their latest revisions last December. The IEA has lowered its previous surplus estimate from 4 million barrels per day (bpd) to 3.8 million bpd, citing production declines in Russia and Venezuela, as well as slightly slower growth from certain non-OPEC+ producers. The EIA predicts a smaller surplus increase, estimating 2.12 million bpd, while BNEF offers a more moderate forecast of 3.2 million bpd.

As we entered 2026, the surplus in the market was gradually taking shape, driven by a slowdown in Chinese stockpiling, which had absorbed much of the surplus in 2025. Brent crude briefly traded below $60 per barrel at the start of the year. However, the downward trend was interrupted by several geopolitical events, which have provided some support to prices.

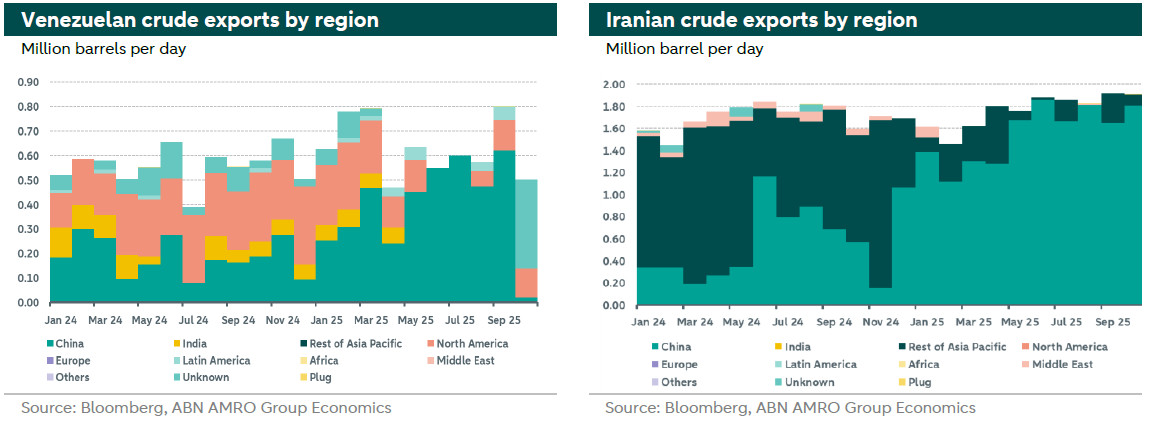

Firstly, the lack of significant progress in peace talks to end the war between Russia and Ukraine has dampened optimism among market participants. As highlighted in our outlook last year (see here), Russia has largely managed to bypass the new U.S. sanctions targeting its two largest oil companies by utilizing its shadow fleet, with China emerging as a key destination. China has taken advantage of substantial discounts stemming from Western sanctions on Russia, Iran, and Venezuela.

Secondly, markets reacted positively to the American intelligence operation that removed the Venezuelan president, following several weeks of U.S. blockade and the seizure of multiple oil cargos. Venezuela's oil production averaged 0.65 million barrels per day (bpd) in 2025, significantly lower than the 3 million bpd it produced a decade ago. The U.S. President announced that the United States would take control of Venezuela's oil industry moving forward, encouraging major American oil companies to invest in the country.

However, these plans face substantial challenges. Years of neglect, corruption, and poor governance have left Venezuela's oil infrastructure in disrepair, requiring an estimated $100 billion in investments to rebuild. Additionally, Venezuelan oil is heavy and sour, resulting in higher costs for extraction and processing. According to Rystad Energy, production costs could range between $45 and $65 per barrel, which is relatively expensive. Furthermore, any new investments by major oil companies are contingent on achieving political and economic stability, especially after previous incidents involving the seizure and nationalization of assets from companies such as ExxonMobil and ConocoPhillips. Accordingly, any changes in output volumes will not big enough to induce a big market reaction for now as lifting production will take time to materialize.

Thirdly, the newly announced 25% U.S. secondary tariffs on countries trading with the Iranian regime have increased supply uncertainty from Iran. Additionally, the market remains cautious about the escalating tensions and U.S. threats to strike the Iranian regime. Such actions could destabilize the region and significantly disrupt oil supplies, particularly those passing through the Strait of Hormuz, which facilitates nearly 30% of the world’s crude oil output. Iran currently produces about 4.2 million barrels per day (bpd), accounting for roughly 4% of global production.

Fourth, the growing tension between the U.S. and the EU over Greenland has further contributed to market uncertainty. The U.S. President has threatened to impose a 10% tariff on several countries starting in February, with plans to raise it to 25% by July if no agreement is reached. In response, the EU is exploring various retaliation strategies (refer to our Top of Mind analysis for details; see here and here). These additional tariffs across the Atlantic could negatively impact economic growth, alter trade flows, and ultimately lead to lower oil demand, exacerbating the existing supply surplus.

As a result, the geopolitical premium has emerged as the primary driver behind the recent increase in oil prices, ranging between USD 4 and USD 7 per barrel. These developments have also reshaped crude oil trade flows, with a significant part of exports from sanctioned countries being redirected to China. Additionally, these events have shifted market sentiment toward a more bullish outlook, as depicted in the right chart above.

Oil market outlook

Based on market fundamentals, the supply glut is expected to continue expanding throughout 2026. However, as the influence of stockpiling on prices diminishes, market dynamics will increasingly hinge on OPEC+ decisions. Thus far, the cartel has followed a strategy aimed at reclaiming market share from other producers such as the U.S., Canada, Brazil, and Guyana. We anticipate that OPEC+ will persist in halting production increases as prices decline, pressuring higher-cost producers to cease production.

For now, we are keeping our outlook unchanged, while recognizing that the market remains highly sensitive to geopolitical developments, which are difficult to predict at this stage and could potentially shift the forecast. The primary supply-side risk stems from escalating tensions in the Middle East, which could amplify the current geopolitical premium. In a scenario involving the closure of the Strait of Hormuz, oil prices could surge by as much as 50%. On the demand side, the outlook may shift significantly if tensions between the U.S. and the EU deteriorate further and reach a stalemate. We summarize below our outlook for Brent in the coming quarters.