Global Monthly - Orange is the new Green

Geopolitical risk is increasingly dominating the outlook. The US-EU dispute over Greenland threatens a new tariff war – or worse. Over the next month, we will see just how far Trump is prepared to go to obtain Greenland, and whether Europe can stand its ground. We refrain from changing our base case given the fluidity of events, but uncertainty is clearly back with a vengeance, and the outlook less benign. Spotlight: We present a framework to analyse the main channels through which geopolitical risk impacts the economy.

Global View: Will Trump risk losing a continent to gain an island?

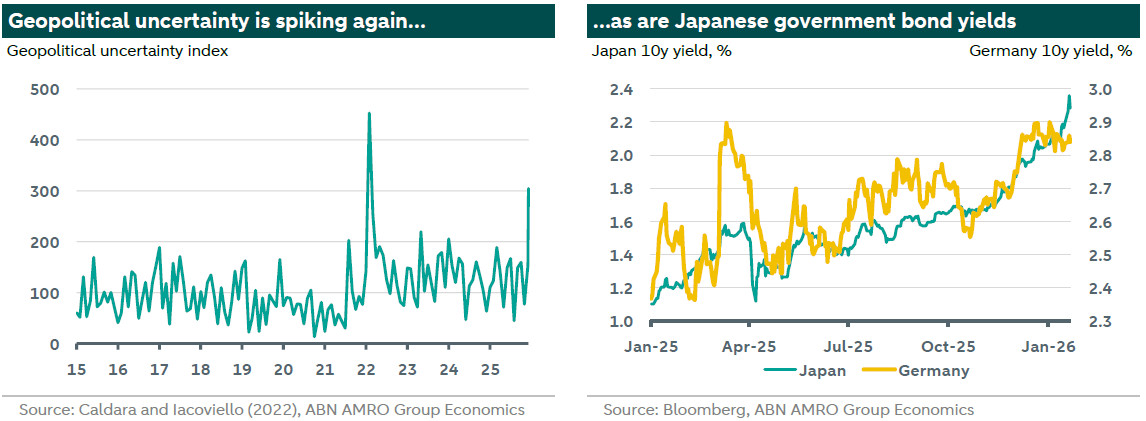

2026 has started off not just with a bang, but with multiple bangs, and we are barely one month in. Geopolitical risk has spiked, reflecting events in Venezuela, Iran, and now most spectacularly the transatlantic dispute over Greenland. Over the coming month we will learn: 1) whether Trump really meant his 10% tariff threat over Greenland (1 February), 2) whether the EU has allowed its suspension of retaliatory tariffs on EUR93bn of US imports to lapse (6 February), and 3) whether the Supreme Court has ruled much of Trump’s tariffs to have been unlawful – potentially leading to refunds of over $130bn in tariffs paid so far. This is just to give a flavour of the uncertainty facing the global economy right now, and this is before we discuss the risk of geopolitical flashpoints escalating militarily, or the volatility in bond and FX markets. Indeed, as if it were not hard enough to translate all of this geopolitical risk to macroeconomic outcomes – a topic we tackle in this month’s spotlight – financial markets threw another curve ball this week in the form of spiking Japanese government bond yields, which threaten to spillover to European government bond markets, and a renewed selloff in the dollar. Are there any crumbs of comfort amid the chaos? The end of the data drought in the US after the government shutdown is finally bringing some visibility US economic performance, though the data so far is unfortunately not yet telling a clear story. And in Europe, the domestic economy is continuing to recover, while France looks like it may avoid snap elections this year after all. Given the fluidity of events, we refrain from reacting with substantial changes to our base case this month. But uncertainty has clearly come back with a vengeance, and the outlook is looking less benign than it did at the end of 2025.